While it is not usual for us to make comment on short-term market events, we have had many inquiries—‘what is going on in the markets right now?’ and ‘have we seen the worst of it yet?’.

It is a very difficult market environment to read at the moment. All major financial markets (shares, bonds, currencies and commodities) are jumping wildly (up and down) at the news cycle, and there is much erratic behaviour feeding the volatility e.g. central banks rapidly hiking interest rates led by the Federal Reserve, major uncertainty around inflation data on a monthly basis, the United Kingdom (UK) tax cuts and Bank of England quantitative easing (QE) policies; and then reversal, an Organisation of the Petroleum Exporting Countries (OPEC) meeting with an agenda to potentially cut oil production and the Ukraine War situation, because it is heavily dependent on what Putin does next.

Equity markets are currently seeing bad news regarding the economy as good news for the market. They are being buoyed by any data announcement that is pointing to economic softness, as this increases the prospect that Central Banks won’t push as hard with increasing policy rates. Conversely, good news such as low unemployment, has been seen negatively by the market, as it indicates that Central Banks will continue to hike.

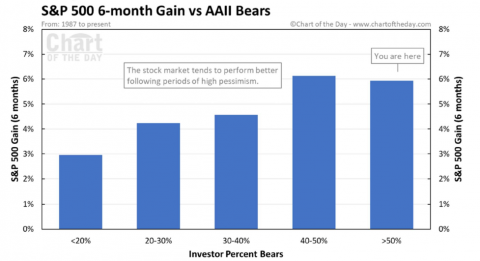

In an environment like this, the bottom will only be evident in hindsight. The observation I make, and somewhat uncomfortably given how fluid the situation is at the moment, is that it appears that there is a lot of bad news already in the market price (see chart below).

From this chart it is worth noting:

The highest percentage of American Association of Individual Investors (AAII) bearish sentiment was 70% and occurred on 5 March 2009, near the end of the global financial crisis bear market.

The lowest percentage of AAII bears was 6% on 21 August 1987, shortly before the stock market crash of October 1987.

The key question is now if it is all in the price? From what we are seeing, maybe not all, but most. Earnings Per Share (EPS) revisions have not yet been revised down to the extent one would expect given the increased prospect of recession and retail sales, while off their highs, have remained resilient. Continuing to quote conflicting data, ad nauseam, would only serve to highlight how difficult it is to make sense of the markets and the economic prospects in the near term.)

From market activity in the past two weeks in particular, the swings are of a significant magnitude. Currently, +/-1% is not a significant move in the present market environment. This behaviour is characteristic of an inflection point (not a turning point); meaning, it could turn and rebound higher or it could leg down again.

The Reserve Bank of Australia’s (RBA) October monetary policy announcement is a case in point. The markets were expecting a rise of 0.50% in the cash rate, but the RBA delivered only a 0.25% increase. This indicates a softening in the RBA’s position regarding inflation. Time will tell, though this is the first time since the beginning of the tightening cycle that the RBA has eased the pace.

The material on this website has been prepared for general information purposes only and not as specific advice to any particular person. Any advice contained on this website is General Advice and does not take into account any person's particular investment objectives, financial situation and particular needs. Before making an investment decision based on this advice you should consider, with or without the assistance of a securities adviser, whether it is appropriate to your particular investment needs, objectives and financial circumstances. In addition, the examples provided on this website are provided for illustrative purposes only. Although every effort has been made to verify the accuracy of the information contained on this website, Infocus, its officers, representatives, employees and agents disclaim all liability (except for any liability which by law cannot be excluded), for any error, inaccuracy in, or omission from the information contained in this website or any loss or damage suffered by any person directly or indirectly through relying on this information.